Key Points

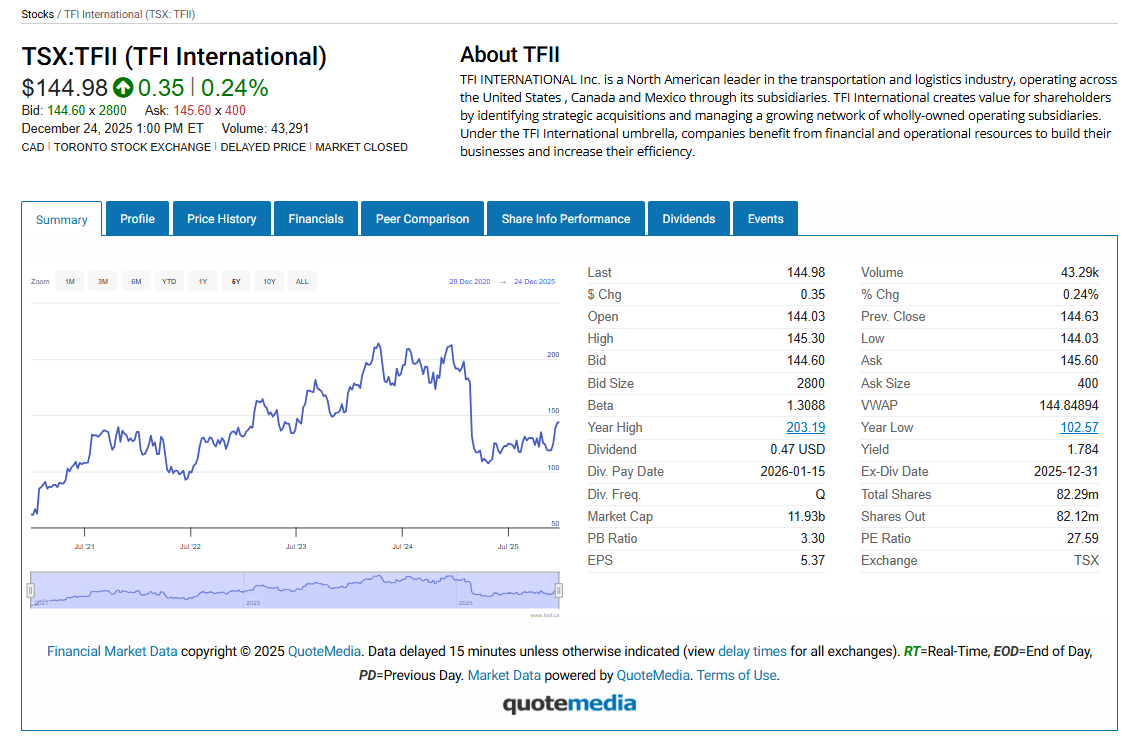

TFI International moves freight across North America. Q3 2025 revenue fell 10% to $1.97B and EPS to $1.20. Upside depends on freight stabilizing and U.S. LTL execution.

The market loves to punish good businesses when a cycle turns, and that’s exactly when long-term passive-income investors can find their best buys. A dividend stock can drop for reasons that have nothing to do with a broken model, like weaker demand, higher rates, or one rough quarter that spooks everyone. If the dividend stock still generates steady cash, protects the balance sheet, and keeps the payout sensible, a lower share price can hand you a better entry point and a higher starting yield. Your job is to tell the difference. That’s where value often hides.

Consider TFII

TFI International (TSX:TFII) fits the boring but important bucket that often works for patient investors. It moves freight across North America through less-than-truckload, truckload, and logistics operations, and it has built scale through years of acquisitions. Freight never wins popularity contests, yet the economy runs on it. When retailers restock, factories ship, and e-commerce hums, TFII sits in the middle and takes a cut. It also has a shareholder-friendly streak, with regular dividends and share buybacks when conditions allow. Even with those strengths, the dividend stock has looked bruised over the last year. At writing, recent performance data shows TFII down about 32% from a year ago. The shares have also bounced at times, which tells you investors still see quality under the hood. For a buyer, that mood swing can create value, especially when the underlying network and customer base still look durable. And right now could be an interesting time, considering shares have risen 21% in the last month alone.

Into earnings

The latest earnings explain why investors have acted cautiously, and also why they might come back around. In its third-quarter 2025 report, TFI posted revenue of $2 billion, down 10% year over year, and adjusted diluted earnings per share (EPS) of $1.20, also below the prior-year quarter. Freight demand has cooled, and softer volumes show up quickly in this industry, especially in the places where pricing power fades first. That creates a messy stretch where strong operators still look weak on paper. But the same report also shows why income-minded Canadians still keep TFII on the list. The board approved a 4% dividend increase, lifting the quarterly dividend to US$0.47 per share. Dividend growth rarely survives if cash flow can’t support it. On valuation, major market data still puts the dividend stock trading at 27 times earnings, which can look reasonable for a quality operator in a weak part of the cycle.

Looking ahead

So why can TFII look like a buy even when it’s down? First, freight cycles turn. When demand stabilizes, a well-run carrier can rebuild margins and cash generation faster than the headlines change. Second, TFII doesn’t need a perfect economy. It needs normal performance, plus steady execution in the parts of the business investors scrutinize most closely. Meanwhile, the dividend gives you tangible progress while you wait. The catalysts don’t need fireworks. You just need the freight cycle to move from worse to improving, plus steady execution in the U.S. LTL business that investors watch closely. If that happens, the market can start valuing TFII like a durable operator again, not a story that has lost its edge. The dividend then becomes a bonus on top of a recovery, rather than the only reason you own it. The risk stays real, too, of course. Freight can stay weak longer than you want, wages and fuel can pressure margins, and integration missteps can sting.

Bottom line

If you want a dividend stock that still offers real upside, TFII makes a clean case as a patient buy. A TFSA wealth plan rewards time, not timing, and TFII still runs an essential network, still generates real cash, and still raises its dividend. If you can hold for years, not months, buying while the market pouts can become the move you feel smartest about later.