Key Points

Fortis and Manulife are poised for success in 2026 with Fortis offering defensive dividend growth and Manulife benefiting from strong life insurance and wealth management business in Asia. Caution is advised with Lightspeed Commerce due to its declining stock value and potential need for more capital, marking it as a risky investment.

Given the fact that we’re about to turn the page to a New Year, investors may be rethinking how robust their portfolios are and whether they can withstand any sort of major market headwinds over the course of the next 12 months. Of course, predicting just what sort of bullish catalysts or bearish headwinds may arise over the next year is nearly impossible. Outside of AI (and the bull/bear case around this pivotal technology), there really aren’t many areas where predictions will be helpful. For example, I have no idea where interest rates, commodity prices, and other key inputs will end next year. With that said, given the current underlying dynamics in the market, here are two stocks I think could have a big year next year regardless of the macro backdrop, and one I believe is not well-positioned to handle whatever is ahead.

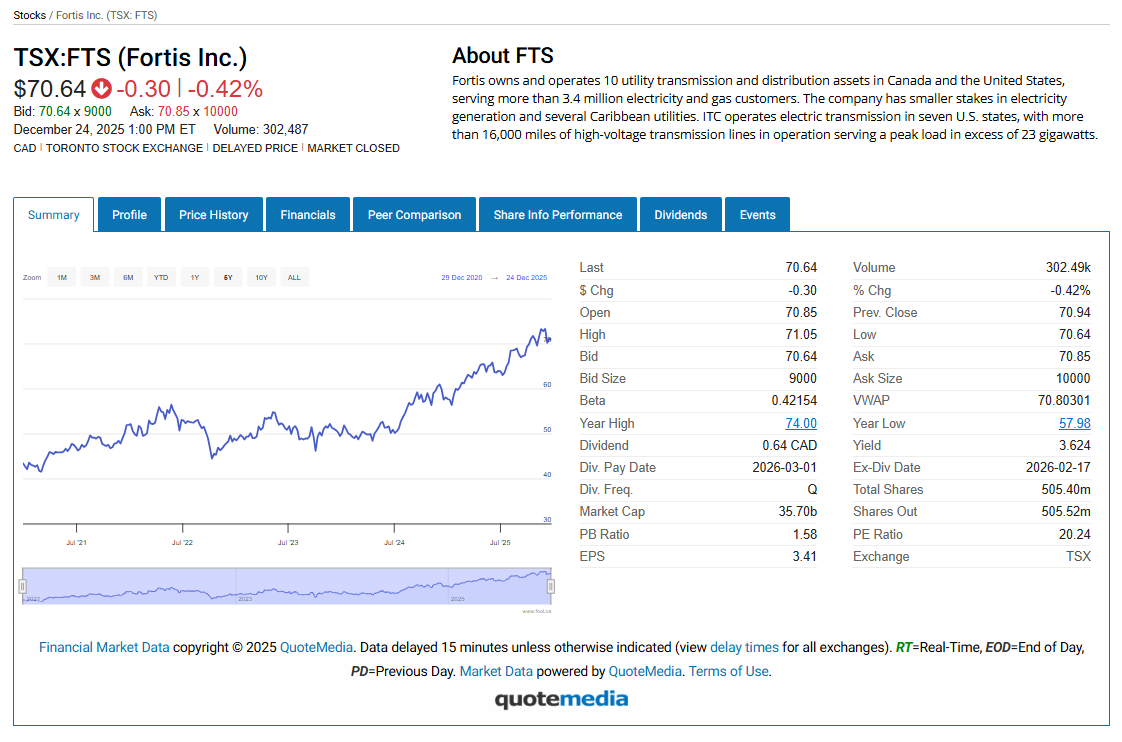

Buy: Fortis

One of the top dividend growth stocks in the market and a company I think can continue to deliver growth in 2026 and for decades to come, Fortis (TSX:FTS) is among my most defensive stock picks for the coming year, for investors with a long-term investing time horizon. That’s primarily due to the fact that, as a key regulated utilities provider of electricity and natural gas to millions of residential and commercial customers, Fortis’ business model really is acyclical. In other words, no matter what happens with the broader economy, the AI buildout is underway, and existing customers will have no choice but to pay their Fortis bills to keep the lights and heat on. That cash flow stability and potential for dividend growth are what have kept Fortis’ dividend yield relatively low at just 3.6%. That said, I think the company’s long-term capital appreciation upside should make for high single-digit or low double-digit annual returns. In a potentially volatile year, that’s good enough for me.

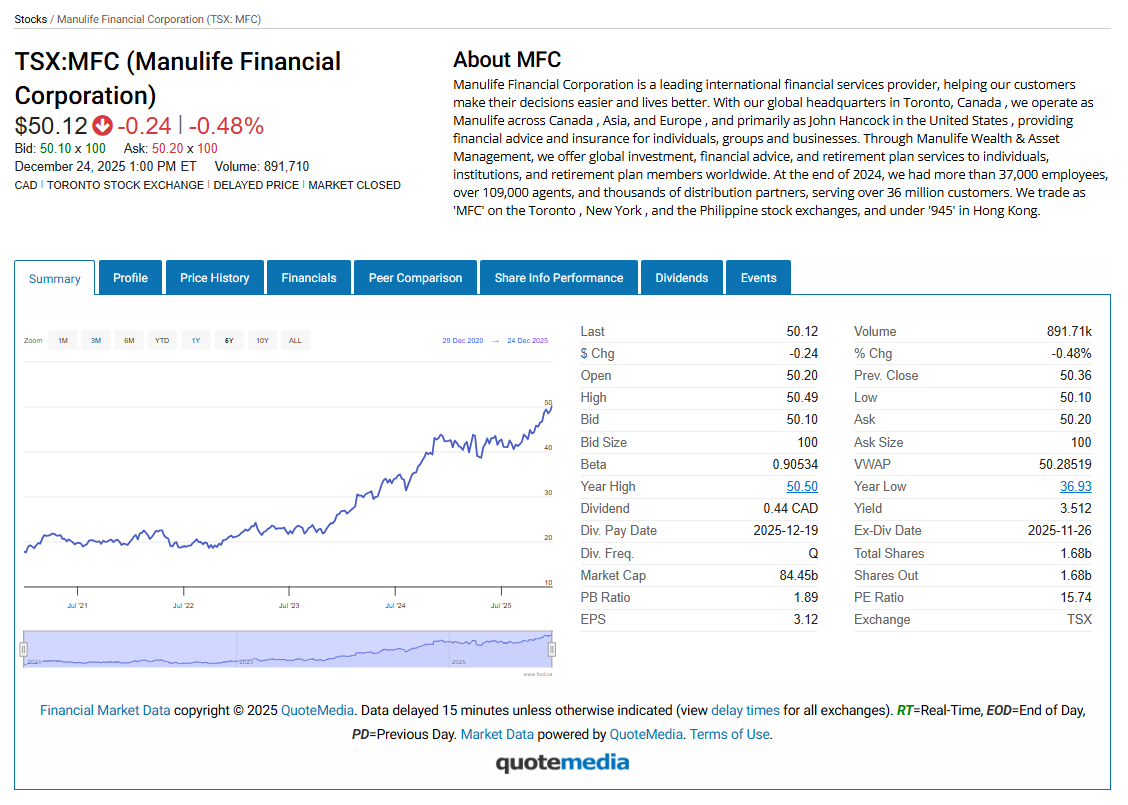

Buy: Manulife

Few sectors are as defensive as life insurance, and in this sector, Manulife (TSX:MFC) is among the best options for Canadian investors looking for upside right now. The company’s core life insurance business has remained solid, and Manulife has posted increasingly strong results in recent quarters, supported by higher yields on longer-duration assets. Like other insurers, Manulife needs to match up its longer-duration liabilities with assets that pay out over longer periods of time (such as bonds), so lower yields, or even expectations of lower long-term yields, have boosted the company’s outlook in this regard. On top of this underlying strength, the company’s wealth management business is also surging. That’s come mostly due to the company’s growth strategy in Asia, and that’s key to my long-term thesis in this name. With an 18% year-to-date return in its shares and a 3.5% yield, investors have pulled in more than a 20% total return this year. While 2026 may not bring about such rosy numbers, it could still be a very profitable year for investors in this name in my view.

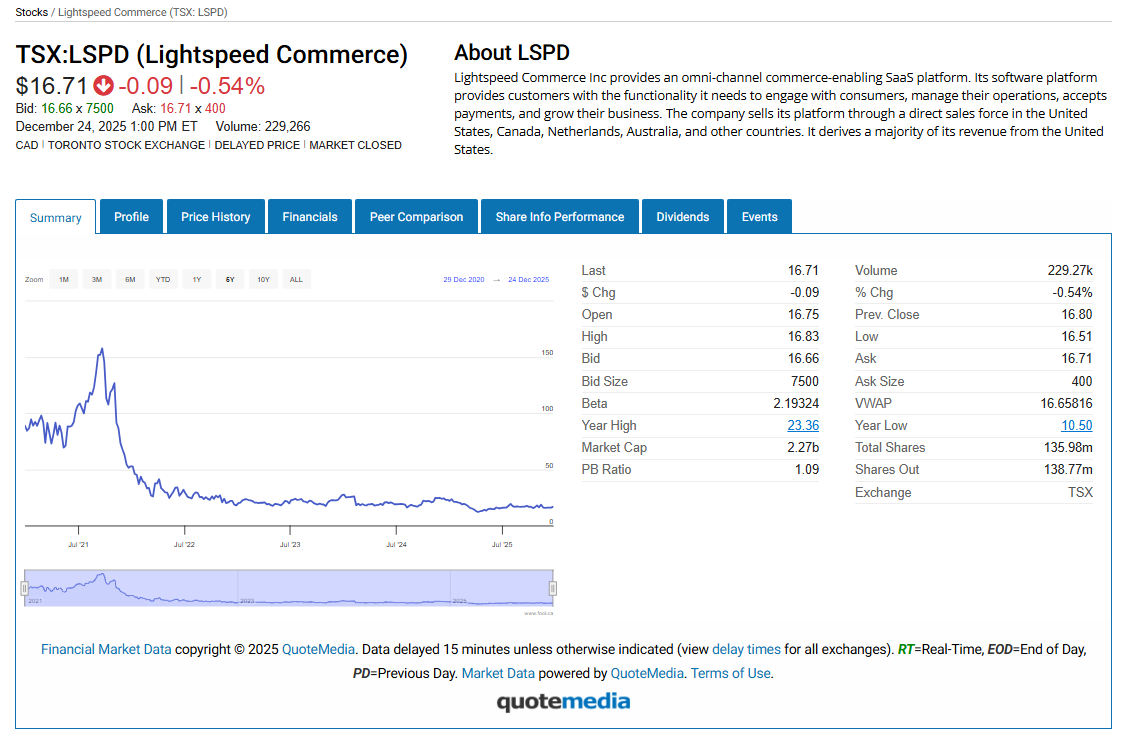

Sell: Lightspeed Commerce

One Canadian growth stock I’ve become more bearish on of late is Lightspeed Commerce (TSX:LSPD). Shares of the Canadian tech stock have been absolutely decimated in recent years, as its rollout of point-of-sale software and numerous strategic shifts have not paid off. I previously discussed this stock as very overvalued during the 2021 boom, which saw shares surge to more than $150. Now trading around $16.50 and down 25% since the beginning of the year, this is a stock I don’t think investors want to step in front of, particularly if valuations in the tech sector continue to come down. At some point, I think Lightspeed may need to raise more capital to stay afloat, and it’s not growing like investors clearly had hoped. This is one Canadian tech stock I wouldn’t personally touch with a 10-foot pole, but that’s just me.