Key Points

Despite impressive gains for equity investors since the market bottomed in 2022, signs such as geopolitical concerns and slowing job growth suggest a potential bear market in 2026. To protect portfolios, investors can consider defensive stocks like Hydro One, Alimentation Couche-Tard, and Enbridge, which offer stability and growth potential in volatile markets.

The past three years (including 2025) have been incredible for equity investors. After markets bottomed in 2022, the ensuing gains have positively benefited investors all around the world (with very few exceptions) who have stayed invested through the recent volatility. And while there are plenty of voices on Wall Street and elsewhere who continue to tout 2026 as a likely extension of this ongoing bull market, the reality is that some cracks are showing underneath the surface. Whether we’re talking about geopolitical concerns, shifting trade policies, or slowing job growth in major economies around the world, some signs are pointing to a potential bear market starting in 2026. For those looking to protect their portfolios from such risks, here are three ideas for how to manage through a potentially volatile year.

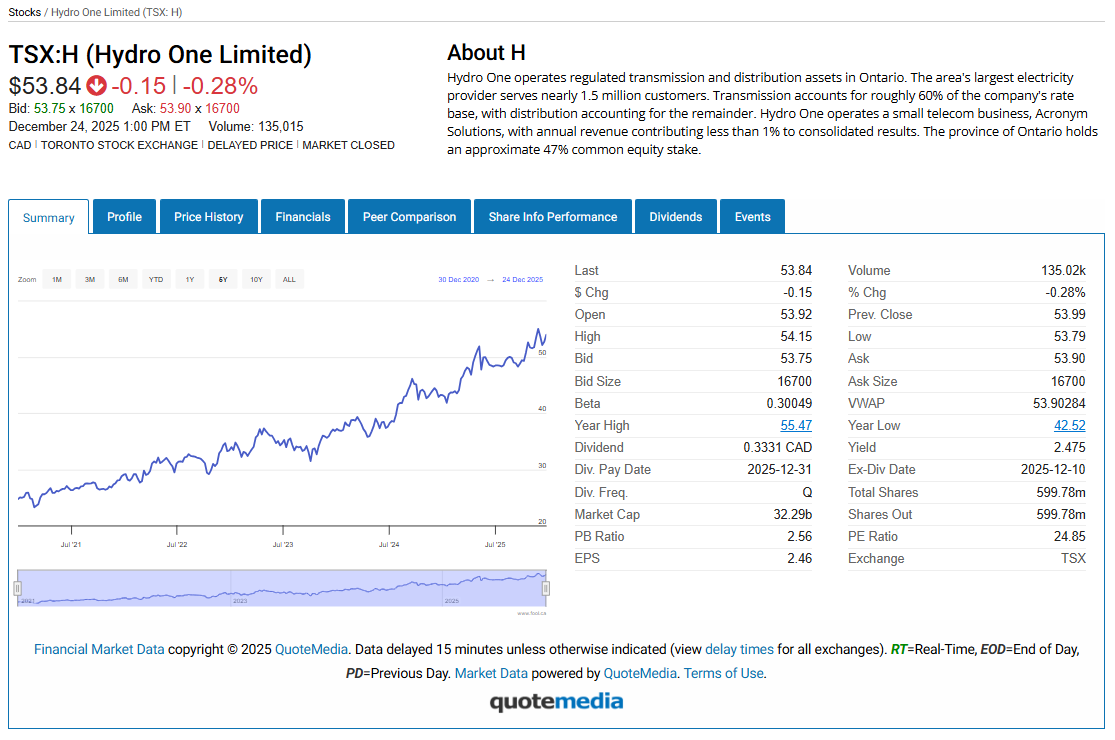

Hydro One

In general, I’m very bullish on the utilities sector as one that can not only survive but also thrive in a market downturn. Hydro One (TSX:H) is one way to play such trends in the Canadian market. Focused on the Eastern Canadian provinces, Hydro One has seen solid growth in recent years. Its balance sheet remains robust, and with a current yield of 2.5% (brought lower by strong capital appreciation in recent years), this is a dividend stock that’s starting to look like a growth stock. Don’t get me wrong, I think Hydro One still likely has plenty of growth potential. That’s partly because I think Eastern Canada could be where many data centres are ultimately built, providing a much more robust revenue and earnings growth trajectory for the company over time. But it’s this company’s ultimate cash flow stability and dividend growth profile that stand out to me as reasons to own this stock long term. On any meaningful dips in 2026, I think Hydro One stock is a screaming buy.

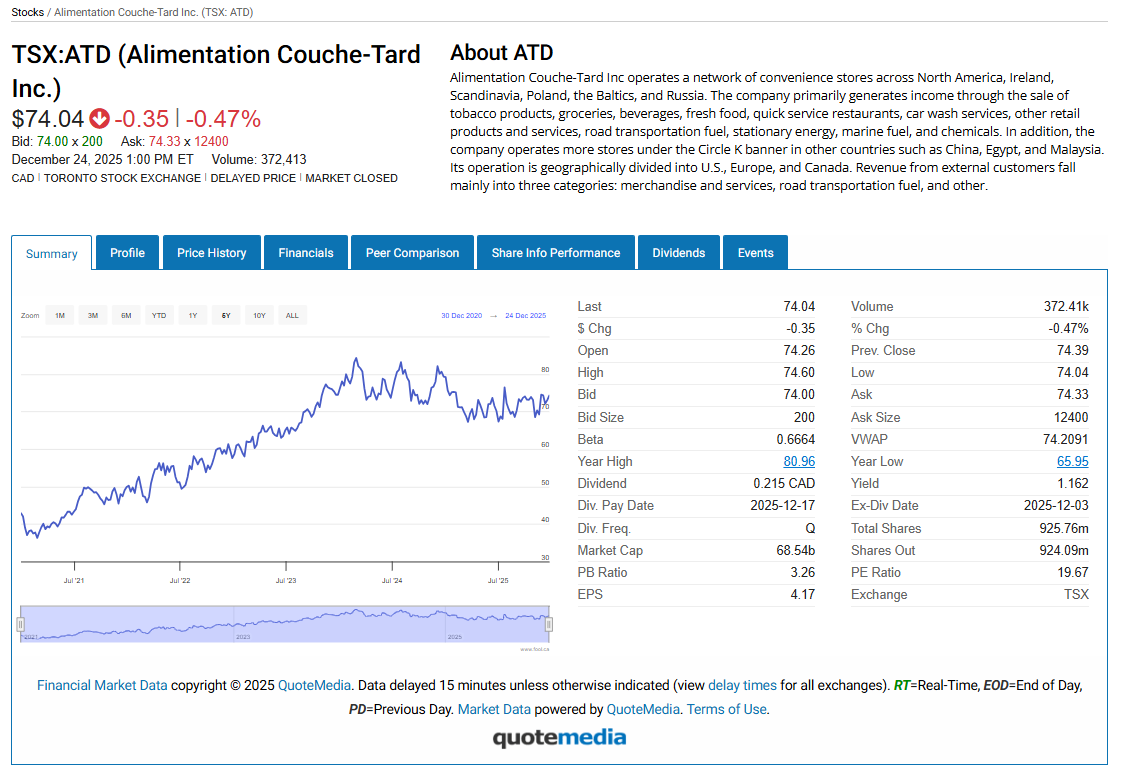

Alimentation Couche-Tard

Another defensive stock I’ve touted as a value play in the past, Alimentation Couche-Tard (TSX:ATD) looks well-positioned to ride any negative bear market headwinds toward highs. If capital begins to rotate into more defensive areas of the economy, I think there’s a case to be made that owing Couche-Tard stock here makes sense. After all, demand for gas stations and convenience store purchases won’t meaningfully decline in downturns. We’ve seen how these dynamics have played out in the past. With a dividend yield of 1.2% and a forward price-earnings ratio of just 18 times, I still think ATD stock is cheap here, even after its rise in recent years.

Enbridge

Another company with a business model that has little to do with the overarching macro backdrop is Enbridge (TSX:ENB). Shares of this leading North American pipeline company have been on a tear in recent years, surging toward a level that’s approaching its all-time high back when oil prices spiked in the mid-2010s. That’s impressive, since that was the last time interest around pipeline growth was prominent. Today, many of those same tailwinds are at play once again. Thus, from a dividend perspective (an impressive 6% yield is reason enough to own this stock) to its growth tailwinds, I think this is a stock that can grow through any near-term market turmoil we may see in the year to come.